Europe Machine Learning Market Size

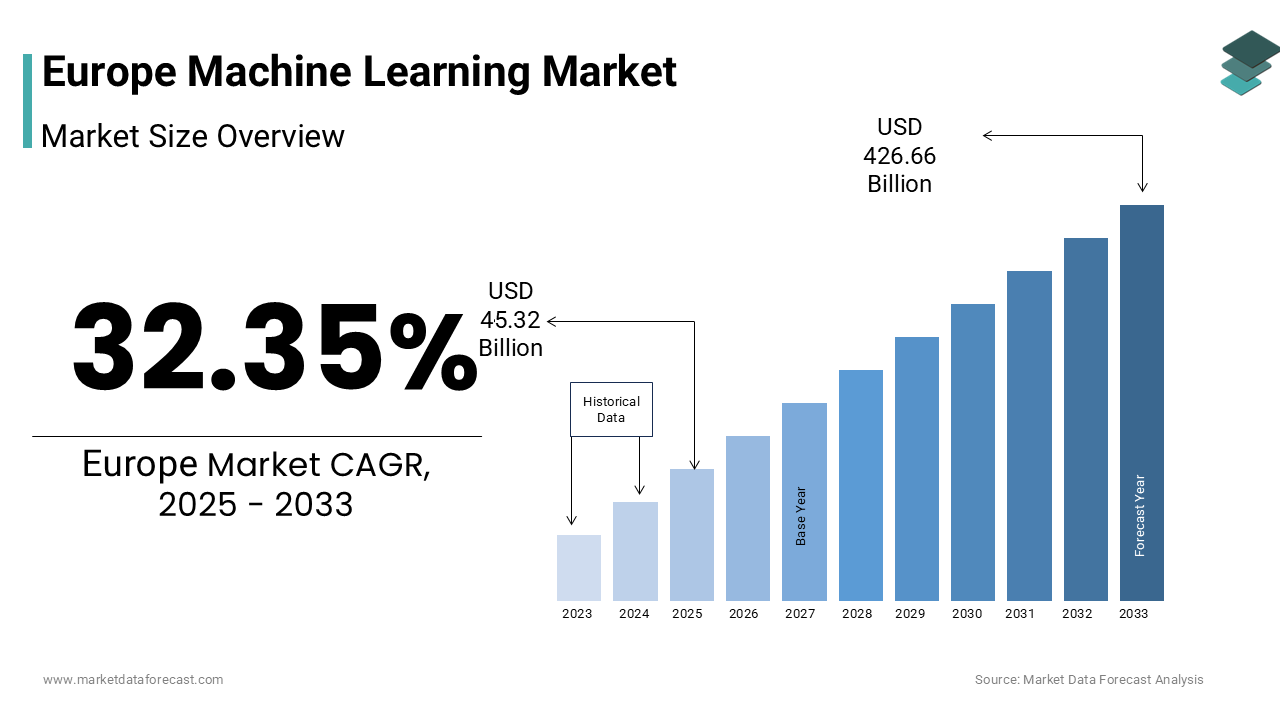

The Europe machine learning market size was valued at USD 34.24 billion in 2024 and is anticipated to reach USD 45.32 billion in 2025 from USD 426.66 billion by 2033, growing at a CAGR of 32.35% during the forecast period from 2025 to 2033.

Machine learning is an algorithmic system that enable computers to learn from data patterns and improve performance without explicit programming. These technologies span supervised unsupervised and reinforcement learning models applied across healthcare manufacturing finance and public services to automate decisions optimize processes and extract predictive insights. Unlike generic artificial intelligence the machine learning segment specifically emphasizes statistical inference and adaptive computation grounded in empirical data. According to Eurostat, about 13.5% of enterprises in the European Union used at least one artificial intelligence technology in 2024. Many large enterprises have adopted AI tools for operational analytics and decision-making. Europe hosts a vibrant ecosystem of AI and machine-learning-driven startups. Financial institutions across the euro area are increasingly using machine-learning techniques for credit-risk assessment and fraud detection. Public agencies and environmental observatories in Europe leverage machine learning models to process large volumes of satellite and sensor data for climate forecasting and environmental monitoring. These institutional adoptions reflect a structural shift toward data-driven governance and industrial automation across the continent.

MARKET DRIVERS

Regulatory Push for AI Governance Accelerating Enterprise Adoption

The Artificial Intelligence Act of the European Union has catalyzed responsible machine learning deployment by establishing a risk-based compliance framework that encourages transparency and accountability, which is one of the key factors driving the growth of the European machine learning market. As the world’s first comprehensive AI law it mandates rigorous documentation model explainability and human oversight for high-risk applications in sectors like healthcare transport and law enforcement. According to the European Commission, a significant majority of large European firms initiated internal governance protocols for machine-learning systems in 2024 to align with emerging regulatory requirements. This legal clarity has reduced perceived adoption risk and spurred investment in auditable model architectures. According to the European Banking Authority, many EU banks now prioritise interpretable machine-learning models for credit-scoring to satisfy regulatory scrutiny. Moreover, the European Data Protection Board issued guidelines in early 2025 requiring data lineage tracking for all training datasets used in public-sector algorithms. These measures have fostered trust among both public institutions and private enterprises. As per a survey by the Centre for European Policy Studies, many European CIOs cited regulatory certainty as a key factor in expanding machine-learning budgets. Far from stifling innovation, the Artificial Intelligence Act is structuring a sustainable ecosystem where ethical and technical rigor drive competitive differentiation.

Talent Shortage and Fragmented AI Education Pathways

Despite strong institutional demand, Europe faces a critical shortage of machine learning specialists capable of designing deploying and maintaining advanced models, which is one of the significant restraints to the growth of machine learning market in Europe. According to the European Centre for the Development of Vocational Training there were reports of very large numbers of unfilled AI-related positions across the EU in 2024 with machine learning engineers among the most-scarce profiles. This gap stems from fragmented higher education curricula where a minority of computer science programmes in EU universities offer dedicated machine learning courses. National disparities further exacerbate the issue with some countries’ tech firms struggling to recruit local machine learning talent and increasingly relying on international hires, and others experiencing emigration of AI graduates. Without coordinated upskilling initiatives and standardised certification frameworks this human-capital deficit will constrain model innovation and deployment velocity. Even leading research institutions acknowledge that talent scarcity is now a primary bottleneck to scaling machine-learning applications across European industry.

MARKET OPPORTUNITIES

Integration of Machine Learning in Green Transition Technologies

The commitment of Europe to climate neutrality by 2050 is creating high impact opportunities for machine learning in energy optimization and environmental monitoring. The European Green Deal explicitly endorses AI driven solutions for smart grids circular economy analytics and emission tracking. Machine learning models are increasingly used across Europe to process data from air-quality sensors and predict pollution hotspots in near-real-time. The energy sector likewise uses machine learning for better forecasting of renewable generation to enhance grid balancing. Industrial decarbonisation programmes have applied machine learning to heavy industries such as cement and steel to achieve meaningful energy efficiencies. In environmental monitoring, deep-learning techniques are integrated into large-scale satellite imagery analysis for land-use change detection. These use-cases demonstrate how machine learning serves as an enabler of regulatory and sustainability objectives, and major European funding programmes now allocate billions of euros to digital-green synergies, which is signalling the convergence of climate policy and algorithmic innovation as a strategic growth frontier for the machine-learning ecosystem.

Expansion of Federated Learning in Privacy Sensitive Sectors

Federated learning is emerging as a breakthrough opportunity for machine learning deployment in Europe’s highly regulated healthcare and finance sectors where data cannot be centrally aggregated. This decentralized approach trains models across distributed devices or institutions while keeping raw data localized thereby complying with the General Data Protection Regulation. According to the European Institute of Innovation and Technology, a pilot involving multiple European hospitals used federated learning to develop a breast-cancer detection algorithm without sharing patient records. According to the European Central Bank, several euro-area banks are collaborating on fraud detection models using federated techniques to reduce false positives. The European Health Data Space initiative further institutionalises this paradigm by mandating privacy-preserving analytics for cross-border medical research. According to the European Telecommunications Standards Institute, a growing number of European fintechs now offer federated-learning-as-a-service for SMEs handling sensitive customer data. This architecture aligns technical capability with Europe’s stringent data-sovereignty principles and creates a unique competitive advantage. With regulatory endorsement and proven efficacy, federated learning is poised to unlock machine-learning adoption in domains previously deemed too sensitive for algorithmic intervention.

MARKET CHALLENGES

Algorithmic Bias and Lack of Standardized Fairness Metrics

Persistent concerns about discriminatory outcomes from machine learning is one of the major challenges to the growth of the European machine learning market. Without standardized evaluation frameworks biased predictions in hiring credit scoring or public service allocation can reinforce systemic inequities. As per a report by the European Fundamental Rights Agency, machine-learning tools used in social welfare eligibility assessments in several EU member states exhibited significant disparities against non-native applicants. The absence of mandatory fairness benchmarks means such flaws may go undetected. While the AI Act requires bias mitigation for high-risk systems, it does not prescribe uniform testing protocols. As per an analysis by the Joint Research Centre, only a minority of public-sector machine-learning deployments included third-party bias audits. Moreover, training data often lacks representation of Eastern and Southern European populations that is potentially reducing model accuracy for these groups. Until Europe adopts harmonised fairness metrics and inclusive data-collection mandates, trust in algorithmic decision-making will remain fragile particularly in sensitive civic domains.

Energy Intensity of Model Training and Environmental Accountability

The computational demands of large-scale machine learning models conflict with Europe’s stringent climate commitments creating a sustainability paradox, which is further challenging the expansion of the European machine learning market. According to studies, training a large-language model can consume around 1,287 MWh of electricity, equivalent to the annual consumption of about 120 average US homes. Data-centres in the EU accounted for an estimated 1.8–2.6% of the total electricity consumption in 2022. This footprint is set to rise significantly as AI workloads expand. Unlike the United States, Europe lacks consistently abundant low-cost renewable energy near key tech hubs, which is increasing carbon-intensity concerns. Until energy-efficient machine learning becomes a regulatory and operational priority, the environmental cost of algorithmic advancement may undermine Europe’s green leadership narrative.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Enterprise Type, Deployment, End-user Industry, and Region. |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

|

Market Leaders Profiled |

SAP SE, KNIME AG, Software Mind, AI Superior, KONUX GmbH, Shift Technology, DeepL Translator, SS&C Blue Prism, Darktrace, and GfK.. |

SEGMENTAL ANALYSIS

By Enterprise Type Insights

. The growth of the large enterprises segment in the European market is driven by their substantial data assets mature IT infrastructure and capacity to invest in advanced analytics talent. Large enterprises possess the capital to adopt comprehensive machine-learning solutions across departments including supply-chain management, customer service and predictive analytics. The extensive data infrastructure that provides the high volume and variety of data required to train robust machine-learning models is further boosting the growth of the large enterprises segment in the European market. Additionally, these organisations often have dedicated data-science teams and partnerships with leading AI vendors such as Google Cloud, Microsoft Azure and AWS which further accelerate adoption. As reported by the European Commission in its 2022 Digital Economy and Society Index, 41% of large enterprises in the EU used big-data analytics, a foundational enabler for machine-learning applications.

The SME segment is expected to experience rapid growth over the forecast period and is likely to witness a CAGR of 23.7% from 2025 to 2033. The democratization of machine learning via cloud based no code platforms and targeted EU funding programs is one of the major factors propelling the growth of the SME segment in the European market. The growing accessibility of cloud-based machine-learning platforms that drastically reduce entry barriers is also boosting the growth of the SME segment. Providers such as Microsoft Azure and Amazon Web Services now offer pay-as-you-go ML services allowing SMEs to leverage AI without massive upfront investments. The targeted policy support of the European Union, such as, through research and innovation funding under programmes like Horizon Europe, is also fuelling the expansion of the SME segment in the European market. Furthermore, the proliferation of user-friendly no-code and low-code machine-learning tools has empowered non-technical staff in SMEs to deploy predictive models. Accelerated adoption is further fueled by intensifying competitive pressure and the need for operational efficiency in a tight labour market.

By Deployment Insights

The cloud deployment segment accounted for the largest share of the European machine learning market in 2024. The dominating role of cloud deployment segment in the European market is driven by scalability cost efficiency and seamless access to managed AI services from hyperscalers. Cloud infrastructure is increasingly the default choice for machine-learning workloads in Europe due to the on-demand GPU availability and automated model lifecycle management. Cloud-based machine-learning operations are widely credited with enabling faster experimentation, shorter development cycles and more flexible scaling compared with purely on-premise alternatives. Leading providers such as Amazon Web Services, Microsoft Azure and Google Cloud have established sovereign cloud regions in locations like Frankfurt, Paris and Dublin to address latency, data-residency and regulatory compliance concerns. Many European enterprises using cloud-based AI services report improved retraining frequency and more agile model deployment due to the integrated data pipelines. In sensitive sectors such as health, initiatives like the European Health Data Space leverage federated cloud environments to support collaborative model development while preserving data locality. With both technical and regulatory advantages, the cloud deployment held the dominating role and this trend is likely to continue throughout the forecast period.

The on-premise deployment segment is estimated to grow at a CAGR of 19.9% over the forecast period. The rising data sovereignty concerns in defense finance and critical infrastructure sectors where regulatory mandates prohibit external data processing is primarily propelling the growth of the on-premise segment in the European market. According to the European Defence Agency, many classified machine-learning applications in EU member states must operate in air-gapped on-premise systems to prevent data leakage. Similarly, the European Central Bank mandates that core risk-modeling for systemic banks remains within internal data centres. According to the European Union Agency for Cybersecurity, a significant share of energy and transport operators now deploy on-premise machine-learning for real-time anomaly detection in order to comply with the NIS2 Directive. Advances in edge-AI hardware from firms like NVIDIA and Intel have further enabled high-performance local inference without cloud dependency. Many industrial manufacturers have upgraded on-premise servers to support real-time machine-learning on production lines. These security-driven and latency-sensitive use-cases are contributing to the adoption of on-premise deployment despite the broader cloud shift, which is favouring the expansion of the on-premise segment in the European machine learning market.

By End-use Industry Insights

The BFSI segment commanded the leading share of the European machine learning market in 2024. Financial institutions leverage machine learning for fraud detection credit scoring algorithmic trading and regulatory compliance at scale. According to the European Banking Authority, a large majority of significant EU banks have deployed machine-learning models for transaction monitoring to yield noticeable reductions in false positives. According to the European Central Bank, machine-learning-based systems now process the vast bulk of real-time payment fraud alerts across the euro-area banking sector. Insurance firms also use predictive-analytics tools for claims assessment with several major players achieving materially faster settlement times via automated image-recognition and related methods. Moreover, the Digital Operational Resilience Act compels financial institutions to implement advanced anomaly-detection systems, which is reinforcing investment in machine-learning for risk compliance. As per the European Insurance and Occupational Pensions Authority, many insurers now use machine-learning for dynamic risk pricing based on telematics and behavioural data. This combination of data-rich operational contexts, regulatory impetus and high cost of error are primarily driving the domination of the BFSI segment in the European machine learning market.

The healthcare segment is anticipated to grow at the fastest CAGR of 26.2% over the forecast period owing to the Europe’s aging population diagnostic imaging demands and the European Health Data Space initiative. Machine learning algorithms are increasingly used in radiology departments across the EU for early detection of tumours and neurological conditions. The European Medicines Agency approved multiple AI-based medical devices in 2024 all incorporating machine learning for real-time clinical decision support. National health systems are also investing heavily. For example, France’s national AI in Health strategy allocated hundreds of millions of euros in 2024 to deploy predictive models for hospital-bed optimisation and epidemic forecasting. Similarly, Germany’s Digital Healthcare Act mandates reimbursement for certified AI diagnostics, which is accelerating adoption. According to the National Health Service (UK), machine learning assisted early-warning systems contributed to reductions in sepsis mortality. With regulatory pathways now established and clinical validation advancing, the healthcare segment is expected to exhibit rapid growth in the regional market over the forecast period.

REGIONAL ANALYSIS

Germany Machine Learning Market Analysis

Germany led the Europe machine learning market with a 26.1% of the regional market share in 2024 owing to Germany being a powerful industrial base, strong public research funding and strategic alignment with Industry 4.0. Germany has a vibrant AI research ecosystem via the Fraunhofer‑Gesellschaft that operates around 75 research institutes across the country focusing on applied machine learning among other fields. According to the OECD Artificial Intelligence Review of Germany (2024), the strengths of Germany lie in applied research, transfer to industry and manufacturing use-cases. According to research reports, in Germany a significant increase has been noticed in the adoption of AI among German firms in manufacturing and services in 2024. The structural advantages derived from strong industrial demand, academic excellence and public policy support continue to position Germany as a leading actor in European machine learning market.

United Kingdom Machine Learning Market Analysis

The United Kingdom is another promising market for machine learning in Europe and occupied the second largest share of the European market in 2024. Despite Brexit, the UK maintains a vibrant AI ecosystem anchored by world class universities and a deep fintech corridor. The UK hosts a large and growing number of AI startups, many of which center on machine-learning technologies. The Alan Turing Institute collaborates with NHS England on machine-learning models for genomic medicine and pandemic response. According to a report by the Bank of England, most major UK financial institutions now use AI for market-risk simulation and transaction surveillance. The UK government’s National AI Strategy allocated billions of pounds between 2022 and 2025 to scale AI adoption across public services. In 2024, the Medicines and Healthcare products Regulatory Agency fast-tracked approval of machine-learning-based diagnostic tools. London’s status as a global talent magnet ensures continuous innovation. Regulatory agility and cross-sector collaboration sustain the strong position of the UK in the European machine-learning market.

France Machine Learning Market Analysis

France captured a considerable share of the European machine learning market in 2024. The growth of the French market is majorly driven by the rapid adoption of AI, strong aerospace and luxury sectors and centralized digital health initiatives. France has seen substantial investment in AI research via its national research agency with machine-learning identified as a primary focus area. According to the Interministerial Directorate for Digital Affairs, a majority of French public hospitals now use machine-learning tools for patient-flow optimisation and diagnostic support. Major corporations such as Airbus and LVMH deploy machine-learning for supply-chain resilience and demand forecasting. According to INSEE, while adoption of machine-learning in retail is rising. The French Tech Sovereignty Fund also provides significant funding to scale domestic AI champions like Mistral AI. With coordinated public-private investment and sector-specific use-cases, France is expected to have a lucrative future in the European market over the forecast period.

Netherlands Machine Learning Market Analysis

The Netherlands is predicted to exhibit a prominent CAGR over the forecast period in the European machine learning market owing to the advanced digital infrastructure strong logistics sector and open data policies. The Netherlands has seen substantial enterprise uptake of machine-learning tools, particularly in sectors such as energy optimisation and customer analytics. The Port of Rotterdam Authority employs machine learning to predict vessel arrival times and optimise cargo handling to achieve significant reductions in dwell time. In the financial sector, machine-learning is embedded in many fintech compliance systems for real-time transaction monitoring. The Netherlands also hosts a large number of AI ethics review boards, which is institutionalising responsible deployment. The government’s national AI literacy programmes have trained a broad base of citizens in basic machine-learning concepts. This blend of infrastructural readiness, sectoral innovation and societal engagement are propelling the growth of the Netherlands in the European market.

Sweden Machine Learning Market Analysis

Sweden is anticipated to account for a notable share of the Europe machine learning market during the forecast period. Sweden excels in green tech and digital public services where machine learning drives sustainability and efficiency. Sweden shows strong adoption of machine-learning technologies in sectors such as cleantech and infrastructure. For instance, Vinnova invests heavily in applied AI research and industrial use-cases. The national healthcare and e-health systems utilise shared records feeding machine-learning models for early detection of chronic diseases, and industrial leaders like Ericsson and Volvo Group deploy machine-learning for predictive maintenance and autonomous vehicle training. Local traffic authorities are advancing machine-learning-based solutions for traffic flow optimisation and infrastructure monitoring. Sweden also mandates algorithmic impact assessments for public-sector AI deployments, which is reflecting a commitment to transparency. With high levels of digital literacy, strong R&D investment and a culture of innovation, Sweden maintains a disproportionately influential role in the European machine learning market.

COMPETITVE LANDSCAPE

The Europe machine learning market features a dynamic mix of global technology giants European software vendors and specialized AI startups competing on compliance innovation and sectoral expertise. Hyperscalers like Google Microsoft and Amazon dominate through cloud based platforms offering end to end machine learning workflows yet face scrutiny over data sovereignty. European firms such as SAP and SAS leverage deep regulatory understanding and legacy enterprise relationships to provide auditable and explainable solutions particularly in BFSI and public services. Meanwhile agile startups like Hugging Face and Mistral AI gain traction with open source models and privacy preserving techniques aligned with EU values. Intense competition is further fueled by national AI strategies public funding and talent mobility across borders. Differentiation increasingly hinges on ethical design data governance and integration with existing industrial systems rather than raw algorithmic performance alone. This environment fosters a uniquely European approach to machine learning that balances innovation with accountability.

KEY MARKET PLAYERS

A few of the major companies in the europe machine learning market include

- SAP SE

- KNIME AG

- Software Mind

- AI Superior

- KONUX GmbH

- Shift Technology

- DeepL Translator

- SS&C Blue Prism

- Darktrace

- GfK

Top Players in the Market

Google Cloud

Google Cloud plays a pivotal role in the Europe machine learning market through its scalable AI platform Vertex AI which enables enterprises to build deploy and manage machine learning models with minimal infrastructure overhead. The company has strengthened its European presence by opening dedicated AI research labs in Zurich and Paris focusing on natural language processing and climate modeling. In 2024 Google Cloud launched sovereign AI zones in Germany and France ensuring data residency and compliance with the EU AI Act. It also partnered with major European healthcare institutions to develop federated learning solutions for medical imaging. These initiatives enhance trust and accessibility while aligning with Europe’s regulatory and ethical AI priorities.

Microsoft

Microsoft significantly influences the Europe machine learning market via Azure Machine Learning and its integration with enterprise software such as Dynamics 365 and Power Platform. The company has invested heavily in sovereign cloud infrastructure with data centers in Sweden Switzerland and the Netherlands to meet strict European data governance requirements. In 2024 Microsoft collaborated with the European Commission on the AI Pact to support voluntary compliance with the AI Act ahead of enforcement. It also launched industry specific machine learning templates for manufacturing and retail tailored to EU regulatory and operational contexts. These actions reinforce Microsoft’s position as a trusted enabler of responsible enterprise AI across the region.

SAS Institute

SAS Institute maintains a strong foothold in the Europe machine learning market by delivering highly interpretable and auditable analytics solutions favored by regulated industries such as banking insurance and public administration. Headquartered in the United States SAS has operated European R and D centers in the UK France and Poland for over two decades. In 2024 SAS enhanced its Viya platform with native support for the European Union’s standardized AI documentation requirements under the AI Act. It also launched a machine learning governance toolkit co developed with European financial regulators to ensure model transparency and bias detection. These efforts position SAS as a leader in compliant and explainable AI for high risk applications.

Top Strategies Used by the Key Market Participants

Key players in the Europe machine learning market prioritize regulatory alignment through proactive adoption of the EU AI Act’s requirements including risk classification data governance and human oversight mechanisms. They invest in sovereign cloud infrastructure to ensure data residency and compliance with the General Data Protection Regulation. Many firms develop industry specific machine learning templates for healthcare finance and manufacturing to accelerate deployment. Strategic partnerships with academic institutions and public agencies foster innovation and talent development. Companies also emphasize model explainability and bias mitigation to build trust in high risk applications. Additionally they expand federated and edge learning capabilities to address privacy and latency constraints. These strategies collectively enhance competitiveness while meeting Europe’s unique ethical and operational standards.

RECENT MARKET DEVELOPMENTS

- In March 2024, Google Cloud launched sovereign AI zones in Frankfurt and Paris enabling European enterprises to build and run machine learning models with guaranteed data residency and compliance with the EU AI Act.

- In May 2024, Microsoft partnered with the European Commission to co develop an AI governance dashboard that helps organizations self assess conformity with high risk AI requirements under the Artificial Intelligence Act.

- In February 2024, SAS Institute released a machine learning model documentation framework aligned with the European Union’s standardized technical file requirements for high risk AI systems.

- In June 2024, Amazon Web Services expanded its local machine learning training programs across Germany France and the Netherlands in collaboration with national digital skills agencies to address the AI talent gap.

- In January 2024, IBM introduced a federated learning service on its Cloud Pak for Data platform allowing European healthcare providers to collaboratively train diagnostic models without sharing patient data across institutional boundaries.

MARKET SEGMENTATION

This research report on the europe machine learning market has been segmented based on the following categories.

By Enterprise Type

- Small and Mid-sized Enterprises (SMEs)

- Large Enterprises

By Deployment

By End-Use Industry

- Healthcare

- Retail

- IT & Telecommunication

- Banking, Financial Services and Insurance (BFSI)

- Automotive & Transportation

- Advertising & Media

- Manufacturing

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

link